How I Navigated Property Inheritance Without Losing My Mind

Inheriting property sounded like a win—until I faced hidden taxes, family disputes, and market chaos. I felt overwhelmed, confused, and close to making costly mistakes. But after deep research and real moves in the market, I found a clearer path. This is my story: how I turned a stressful inheritance into a smart financial decision, what traps to avoid, and how market trends shaped my choices—straight talk, no jargon. What began as a gift quickly revealed itself as a complex financial responsibility. The house wasn’t just bricks and memories; it was a legal, tax, and emotional puzzle. With no formal training in finance or law, I had to learn fast. This journey taught me that clarity comes not from instinct, but from strategy, timing, and the courage to make hard choices.

The Unexpected Weight of “Free” Property

Inheriting real estate often feels like a windfall—a gift that boosts net worth with no effort. But the idea that inherited property is “free money” is one of the most dangerous misconceptions in personal finance. The moment ownership transferred, I was hit with a wave of obligations I hadn’t anticipated. Legal fees for probate, appraisal costs, and title transfer charges added up quickly, eating into what I assumed would be a clean gain. These expenses are not optional; they are standard requirements in most jurisdictions, and they can total thousands of dollars depending on the property’s location and value. I learned that even before making any decisions about the house, I was already spending money—money I hadn’t budgeted for and didn’t expect.

Beyond the financial burden, the emotional pressure was just as heavy. Family dynamics shifted almost overnight. Relatives who had shown little interest in the property during my parent’s lifetime suddenly had strong opinions about what to do with it. Some urged me to keep it “in the family,” while others pushed for a quick sale to split the proceeds. These conversations were rarely about financial logic; they were rooted in nostalgia, guilt, and unspoken expectations. I realized that inheriting property isn’t just a legal transfer—it’s a social and emotional event that can strain relationships and cloud judgment. The weight of being the “decision-maker” was isolating, especially when I lacked confidence in my financial knowledge.

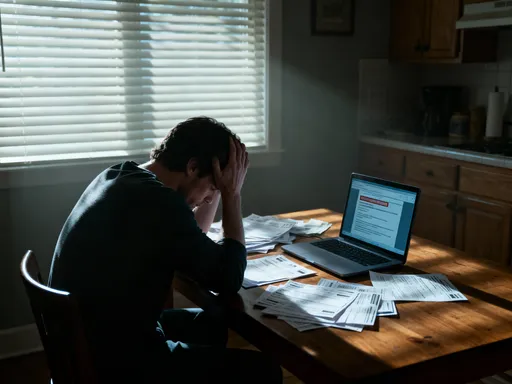

Another shock was the timeline. I assumed I could decide what to do with the house within weeks. Instead, the probate process took months. During that time, the property sat idle, accruing property taxes and maintenance costs. Insurance had to be maintained, utilities kept on, and basic upkeep performed—otherwise, the value could decline. I had to set aside a portion of my own savings just to keep the house in condition, which felt like subsidizing an asset I hadn’t even fully owned yet. This period of limbo was stressful and expensive, reinforcing the truth that inherited property is not a passive gain. It demands attention, resources, and time—three things many heirs, especially those in midlife with careers and families, can’t easily spare.

The lesson here is simple but critical: inherited property is not automatic wealth. It is a responsibility that comes with immediate costs, legal complexity, and emotional labor. Treating it as a prize without assessing the full picture can lead to financial strain and regret. A more realistic mindset is to view the inheritance not as a gain, but as a starting point for a financial decision—one that requires careful evaluation of both tangible and intangible factors. Only by acknowledging the full weight of the situation can an heir begin to make choices that align with their long-term well-being.

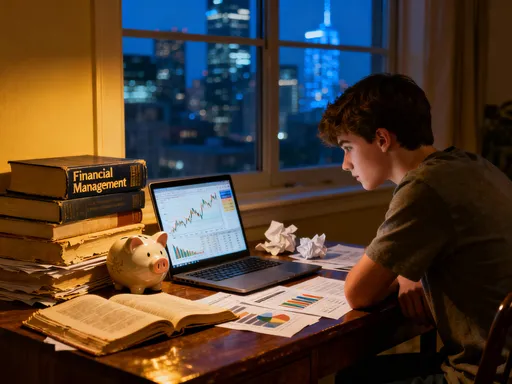

Market Timing: Sell Now or Hold for Tomorrow?

Once the legal hurdles were cleared, the next major decision loomed: should I sell the property now or hold onto it for potential future gains? This choice felt like standing at a crossroads with no clear signposts. On one side was the appeal of immediate liquidity—turning the house into cash that could pay off debt, fund retirement, or support my children’s education. On the other was the possibility of long-term appreciation and rental income, especially if the local real estate market was on an upward trend. The answer wasn’t obvious, and I knew that emotion could easily override logic if I wasn’t careful.

I began by analyzing the local housing market. I looked at home price trends over the past five years, studied vacancy rates, and reviewed planned infrastructure developments in the area. I discovered that while home values in neighboring cities were rising, the neighborhood where the inherited house was located had seen only modest growth. New construction was limited, and the population was aging, which suggested limited demand for rentals or resale in the long term. At the same time, rental prices had increased slightly, driven by a shortage of affordable units. This created a mixed signal: the property might generate steady income, but its long-term value was uncertain.

I also considered my personal financial situation. I didn’t have an urgent need for cash, but I also didn’t want to tie up a large portion of my net worth in a single, illiquid asset. Holding the property meant accepting ongoing risks—market downturns, unexpected repairs, tenant issues—that could erode returns. Selling meant locking in a known value and freeing up capital for more diversified investments. I weighed the opportunity cost: if I kept the house, what other financial goals might I delay? If I sold, could I reinvest the proceeds more effectively elsewhere?

Ultimately, I realized that market timing isn’t about predicting the future perfectly—it’s about making the best decision with the information available. I decided against holding the property long-term because the growth potential didn’t justify the risks and management burden. The market wasn’t crashing, but it wasn’t booming either. This made it a reasonable time to sell—high enough to get fair value, but not so high that I risked missing a peak. By grounding my decision in data rather than emotion, I avoided the common trap of holding onto property simply because it “feels right.” Timing the market perfectly is impossible, but making a thoughtful, informed choice is within reach.

Tax Traps That Catch Even Savvy Heirs Off Guard

One of the most eye-opening parts of the inheritance process was understanding the tax implications. I had assumed that because the property was inherited, I wouldn’t owe capital gains tax when I sold it. That assumption nearly cost me thousands of dollars. While it’s true that inherited property receives a stepped-up basis—meaning the cost basis is adjusted to the market value at the time of death—this doesn’t eliminate all tax liability. If the property appreciated between the date of death and the sale, any gain during that period is taxable. In my case, the real estate market had risen slightly in the months after my parent passed, so I faced a capital gains bill on that increase.

What made this more complicated was the variation in state tax laws. Some states impose inheritance taxes, others have estate taxes, and a few have both. I lived in a state without an inheritance tax, but the property was located in a different state—one that did levy a tax on certain heirs. Fortunately, the value fell below the exemption threshold, so I didn’t owe anything, but I learned how easily this could have been different. Had the house been worth just 15% more, I would have faced a five-figure tax bill. This taught me that location matters not just for market value, but for tax exposure. It’s not enough to understand federal rules; you must also research state and local regulations, which can vary widely and change over time.

I also discovered the importance of tracking improvement costs. When I sold the house, I made several repairs to increase its appeal—roof fixes, painting, and HVAC maintenance. I kept detailed receipts and records, which allowed me to adjust my cost basis upward. This reduced my taxable gain and, consequently, my tax bill. Without those records, I would have paid more. The IRS allows heirs to include certain capital improvements in the cost basis, but only if they’re properly documented. This is a small but powerful way to reduce tax liability, yet many heirs overlook it in the chaos of settling an estate.

To protect myself, I consulted a certified public accountant with experience in estate taxation. This was one of the best decisions I made. The accountant helped me understand the stepped-up basis, identify deductible expenses, and time the sale to minimize tax impact. For example, selling in a lower-income year could reduce the capital gains rate. The cost of professional advice was modest compared to the potential tax savings. This experience reinforced that taxes are not a one-size-fits-all calculation. They require personalized planning, especially when dealing with inherited assets. Ignoring them—or assuming they don’t apply—can turn a seemingly profitable sale into a financial setback.

Renting It Out: Passive Income or Hidden Headache?

Before deciding to sell, I seriously considered renting out the property. The idea of passive income was appealing—monthly checks with little effort. But as I dug deeper, I realized that “passive” is a misleading term when it comes to real estate. Being a landlord involves constant responsibility: finding reliable tenants, handling maintenance requests, complying with local housing laws, and managing cash flow during vacancies. I spoke with friends who owned rental properties, and while some had success, others described sleepless nights dealing with plumbing emergencies or difficult tenants. Their stories made me question whether the income was worth the stress.

I ran the numbers carefully. After estimating rental income, I subtracted property taxes, insurance, maintenance reserves, and potential management fees. The net cash flow was modest—about 4% of the property’s value annually. While not bad, it wasn’t spectacular. More concerning was the volatility: a single major repair, like a new roof or foundation issue, could wipe out a year’s profit. And vacancies weren’t just a loss of income; they also meant continued expenses with no offset. In my area, average vacancy rates were around 7%, but during economic downturns, they could double. This uncertainty made the rental model feel riskier than it first appeared.

I also looked into property management companies. They typically charge 8–12% of monthly rent, plus fees for tenant placement and maintenance coordination. While they could handle day-to-day operations, they wouldn’t eliminate my liability as the owner. I’d still be responsible for major decisions, legal compliance, and financial outcomes. Hiring a manager would make the income more passive, but it would also reduce net returns. And if the manager was unresponsive or unqualified, I could end up with bigger problems than if I had managed it myself.

In the end, I concluded that renting wasn’t the right fit for my lifestyle or goals. I didn’t want to be on call for midnight repair calls, and I didn’t have the time or interest to learn landlord law. The income was decent but not transformative, and the risks outweighed the rewards. For others, especially those with experience or a strong support system, rental property can be a solid investment. But for me, the emotional and logistical burden made it more of a liability than an asset. The dream of passive income often overlooks the reality of active management. It’s essential to assess not just the financials, but also your capacity and willingness to handle the role of a landlord.

The Emotional Side of Letting Go

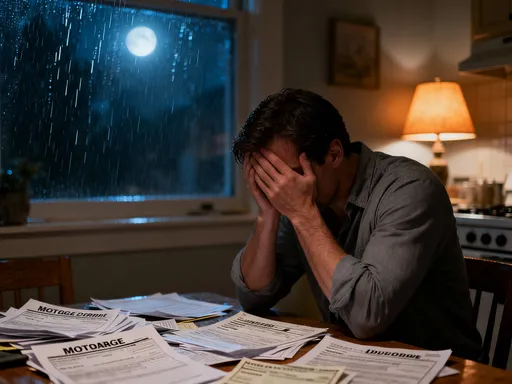

Selling the house wasn’t just a financial transaction—it was an emotional milestone. That home held decades of memories: holidays, family gatherings, quiet mornings with a parent who was now gone. Letting go felt like erasing a part of my history. I struggled with guilt, wondering if selling meant I didn’t value those memories enough. I worried that other family members would see the sale as a betrayal of our shared past. These feelings were powerful, and they threatened to derail my rational decision-making. I realized that sentimentality can be one of the biggest obstacles to sound financial choices in inheritance situations.

I noticed how nostalgia distorted my perception of the property’s value. I began to assign emotional worth to the house, seeing it as irreplaceable and priceless. But that didn’t change the market reality. The house wasn’t a museum; it was an asset with a market price. By conflating emotional value with financial value, I risked holding onto something that no longer served my practical needs. I had to remind myself that keeping the house wouldn’t bring back the past, but it could limit my future. Financial decisions based on emotion often lead to missed opportunities or unnecessary costs.

To manage these feelings, I allowed myself to grieve. I spent a day walking through the house, taking photos, and writing down memories. I created a small keepsake box with mementos—a doorknob, a recipe card, a garden stone. These tangible reminders helped me honor the past without clinging to the property itself. I also talked openly with family members about my decision, explaining my reasoning and listening to their concerns. This didn’t eliminate their disappointment, but it fostered understanding. I learned that emotional closure doesn’t require physical possession. Letting go can be an act of respect, not rejection.

Recognizing the emotional weight of inheritance is crucial. It’s not just about money; it’s about identity, memory, and family legacy. But allowing emotion to dominate the decision-making process can lead to financial strain and long-term regret. The healthiest approach is to acknowledge the feelings, process them, and then make choices based on a balanced view of emotional and financial realities. This doesn’t mean ignoring sentiment—it means not letting it override practical judgment.

When to Call in the Experts (And Who Actually Helps)

Early in the process, I made the mistake of relying on generic advice from well-meaning friends and online forums. While some tips were helpful, others led me down unproductive paths. I quickly learned that not all professionals are equally qualified, and not all advice is created equal. The turning point came when I decided to invest in specialized expertise. I sought out a certified public accountant with estate tax experience, a real estate attorney familiar with probate law, and a local real estate agent with a track record in the neighborhood where the property was located. These individuals provided targeted, actionable guidance that made a measurable difference.

The accountant helped me understand tax implications and identify strategies to reduce my liability. The attorney ensured that all legal documents were properly filed and that I met deadlines for probate and title transfer. The real estate agent gave me an accurate market valuation and advised on timing the sale to maximize returns. Each played a distinct role, and their combined expertise saved me time, money, and stress. I realized that paying for quality advice is not an expense—it’s an investment in better outcomes.

I also learned what questions to ask when choosing professionals. For an estate attorney, I asked how many probate cases they’d handled and whether they specialized in real estate transfers. For a CPA, I looked for certifications and experience with inherited property. For a real estate agent, I checked local market knowledge and recent sales data. Red flags included vague answers, pressure to make quick decisions, or a lack of transparency about fees. I avoided anyone who promised guaranteed results or pushed me toward a specific action without explaining the reasoning.

This experience taught me that expert help is valuable, but only when it’s the right kind of help. It’s not about hiring the most expensive advisor, but the most relevant one. A general financial planner might not understand the nuances of inheritance tax, just as a national real estate chain might not grasp local market dynamics. The right experts bring context-specific knowledge that generic advice cannot match. Knowing when and how to seek their help can transform a chaotic process into a manageable one.

Building a Strategy That Works for Your Future

In the end, selling the property was the right decision for me. The proceeds allowed me to pay off high-interest debt, contribute to my retirement accounts, and set aside funds for my children’s education. More importantly, it gave me peace of mind. I no longer worried about unexpected repairs, tenant issues, or market swings affecting a single asset. The inheritance, once a source of stress, became a foundation for greater financial stability. This experience reshaped my approach to wealth—not as something to hold onto at all costs, but as a tool to build security, flexibility, and freedom.

What I learned extends far beyond one real estate transaction. I now view financial decisions through a broader lens: balancing data with emotion, short-term needs with long-term goals, and risk with reward. I’ve become more proactive about estate planning myself, ensuring that my heirs won’t face the same confusion I did. I’ve also grown more comfortable seeking expert advice and making deliberate choices, even when they’re difficult. The process taught me that financial clarity comes from discipline, not luck.

For anyone facing property inheritance, my advice is this: take a breath. Don’t rush. Educate yourself, consult qualified professionals, and separate emotional attachment from financial reality. Use market data, tax rules, and personal goals as your guideposts. Whether you sell, rent, or keep the property, make the decision with intention, not instinct. Inheritance is not just about receiving something from the past—it’s about shaping your future. With the right strategy, it can be a powerful step toward lasting financial well-being.